The banking strike impact on MSME credit flows in secondary cities is immediate and measurable. Payment cycles slow, loan disbursements pause and working capital stress increases for small enterprises that rely heavily on public sector banking networks.

The banking strike impact on MSME credit flows in secondary cities creates short term liquidity pressure and operational uncertainty for thousands of micro, small and medium enterprises. Unlike large corporations that maintain diversified financing channels, MSMEs in Tier 2 and Tier 3 cities depend primarily on scheduled commercial banks for working capital, term loans and cash management services.

When banking operations are disrupted due to strike action, credit movement slows across the system. For businesses operating on tight margins, even brief interruptions can affect payroll, procurement and vendor settlements.

Working Capital Disruptions for Small Enterprises

Working capital is the backbone of MSME operations. In manufacturing clusters and trading hubs across secondary cities, businesses often rely on cash credit limits and overdraft facilities to manage daily expenses.

During a banking strike, branch operations may be suspended or restricted. Even if digital banking channels remain functional, certain loan processing activities, cheque clearances and documentation based transactions are delayed. For MSMEs that operate on invoice discounting or bill discounting models, this delay disrupts the entire cash conversion cycle.

Secondary cities such as Indore, Coimbatore, Ludhiana and Nagpur host dense MSME ecosystems. In these clusters, supplier payments are closely linked to banking settlement timelines. A slowdown in credit flows can create a ripple effect through the supply chain.

Loan Disbursement and Sanction Delays

The banking strike impact is particularly visible in loan disbursement pipelines. MSMEs awaiting approval for term loans or enhancement of existing limits often face postponements.

Credit committees and branch level sanction authorities may not function during strike periods. This stalls fresh lending. For enterprises planning capital expenditure or seasonal inventory build up, even a few days of delay can alter procurement schedules.

Government supported credit schemes targeted at MSMEs also rely on bank processing. When these channels pause, beneficiaries experience uncertainty. In secondary cities where alternative financing options are limited, dependence on traditional banks remains high.

Digital Banking Versus Physical Branch Dependence

Over the last decade, digital banking penetration has increased significantly. Unified Payments Interface and internet banking have reduced reliance on physical branches for routine transactions. However, MSME credit flows still require physical verification, documentation and relationship management.

In secondary cities, many micro enterprises operate with limited financial formalization. They prefer in person interaction with branch managers for loan negotiations and restructuring discussions. A banking strike interrupts this relationship driven model.

While digital channels ensure that some payment systems continue to function, high value credit decisions are often postponed until full operations resume.

Impact on Supply Chains and Local Economies

MSMEs form the backbone of local economies in non metro regions. They generate employment, supply components to larger industries and sustain service sectors. When credit flow slows, production schedules may be adjusted.

Delayed raw material procurement, postponed dispatches and deferred wage payments can emerge in extreme cases. Although short term strikes rarely cause structural damage, repeated disruptions can weaken business confidence.

In manufacturing heavy secondary cities, where ancillary units support larger industrial plants, liquidity strain can cascade quickly. Timely credit access is therefore not just a financial issue but an economic stability concern.

Alternative Financing Channels and Mitigation

To mitigate the banking strike impact, some MSMEs increasingly explore alternative financing options. Non banking financial companies and fintech lenders provide faster disbursements through digital platforms. Invoice financing marketplaces and peer to peer lending channels are also emerging.

However, interest rates in these segments can be higher than traditional bank credit. For micro enterprises with thin profit margins, cost of capital is a decisive factor. Therefore, while alternatives exist, they are not always preferred.

Diversifying banking relationships is another strategy. Enterprises that maintain accounts across multiple banks may reduce vulnerability during localized disruptions. Yet this requires administrative capacity that smaller units may lack.

Policy and Structural Considerations

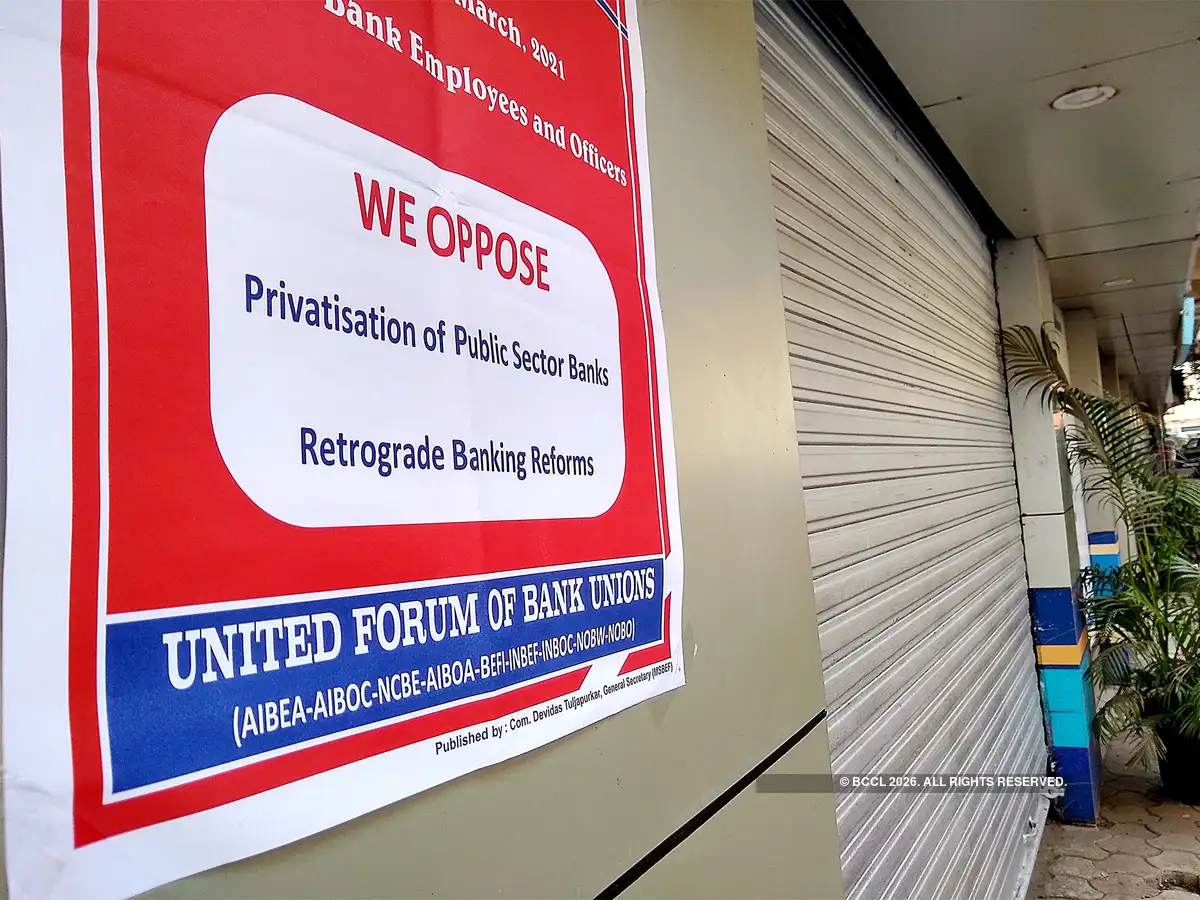

Banking strikes often stem from labor negotiations and policy disagreements. While these are part of industrial relations frameworks, their economic consequences extend beyond the financial sector.

For MSMEs in secondary cities, predictability in credit access is essential. Policymakers frequently emphasize the importance of MSMEs in employment generation and export performance. Ensuring continuity in financial services aligns with that objective.

Long term resilience depends on strengthening digital credit assessment systems, expanding formalization and improving risk based lending models that reduce manual bottlenecks.

Outlook for MSME Credit Stability

In most cases, the banking strike impact on MSME credit flows in secondary cities remains temporary. Once operations normalize, pending transactions are processed. However, the episode highlights structural dependence on traditional banking channels.

As India’s MSME ecosystem continues to expand, especially outside major metros, the resilience of credit infrastructure becomes more critical. Strengthening digital documentation, encouraging financial literacy and promoting diversified financing channels can reduce future vulnerability.

Secondary cities will remain growth engines for manufacturing, trade and services. Stable credit flows are central to sustaining that momentum.

Takeaways

Banking strikes temporarily slow MSME credit flows in secondary cities

Working capital disruptions can affect supply chains and payroll cycles

Digital banking mitigates routine payment issues but not credit approvals

Diversified financing channels improve resilience for small enterprises

FAQs

Q1. How does a banking strike affect MSMEs

Loan processing, credit disbursements and cheque clearances may be delayed, creating short term liquidity stress.

Q2. Are digital payments completely halted during a strike

Most digital systems continue to function, but branch based services and manual approvals can slow down.

Q3. Can MSMEs use alternative lenders during a strike

Yes, fintech lenders and non banking financial companies are options, though costs may be higher.

Q4. Is the impact long term

Typically the disruption is temporary, but repeated strikes can affect business confidence and planning.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment